Owning a small business means making decisions about many types of issues. Some of those decisions include deciding whether or not to hire employees, how much small business insurance to buy, what types of coverage are necessary, and much more.

These types of decisions take research and a proper understanding of the information to know what is best for your small business.

While we cannot help you answer all of your questions, we can help you determine whether a BOP or picking your business insurance a la carte style is the best option for you.

What is a BOP?

A BOP policy is a Business Owner Policy. This type of policy provides small business owners with general liability coverage as well as property insurance.

A BOP is similar to liability coverage for your vehicle. It covers the basics for your business. The general liability covers your customers and others that come into your business should they be injured. It also covers your property should it be damaged.

However, a BOP will not cover damages to you nor damages to your clients due to subpar services or mistakes.

What Types of Small Business Insurance Coverage Are Available?

There are numerous types of coverages available to small business owners. Some coverages protect the basics, and then some coverages extend to protect all other issues a business owner could encounter.

Here are some of the more common small business insurance policies.

Professional Liability Insurance

Professional liability insurance is also known as errors and omissions coverage. This type of coverage protects the small business owner when they or an employee makes an error while performing their normal operations. These types of errors negatively affect clients.

For instance, if you are a house cleaner and you use a chemical that causes damage to your client’s property, your errors and omissions policy will cover the claim.

Worker’s Compensation Insurance

When a small business hires an employee, it becomes responsible for that employee’s well-being on the job.

Worker’s compensation insurance protects the employer and provides for the employee should an accident occur. Depending on the type of business, work comp may be minimal, or it may be quite costly.

For instance, a business that has more risks, such as a construction business or home improvement contractor, will have higher work comp premiums than a law firm. In a law firm office setting, the most significant threat may be slip and fall claims on wet floors.

Property Insurance

If you own a property or rent a property, you need property insurance. This coverage protects the property and its contents from issues such as theft, fire, flood, and any other type of damage.

Depending on the location of your property, you may need additional coverages, such as specific flood insurance policy, in order to make sure your property is covered in the event of any type of damage, including natural disasters.

General Liability Insurance

General liability insurance protects you and your business if someone is injured on your property.

If a person slips and falls in your store or suffers some other type of injury from your business, your general liability insurance can kick in and help protect your assets.

Product Liability Insurance

When your company makes widgets, there are times when the widgets can have a problem. These problems are known as product malfunctions.

Product liability will help protect your company’s assets and your personal assets if that product malfunctions and causes damage or injury to an end user.

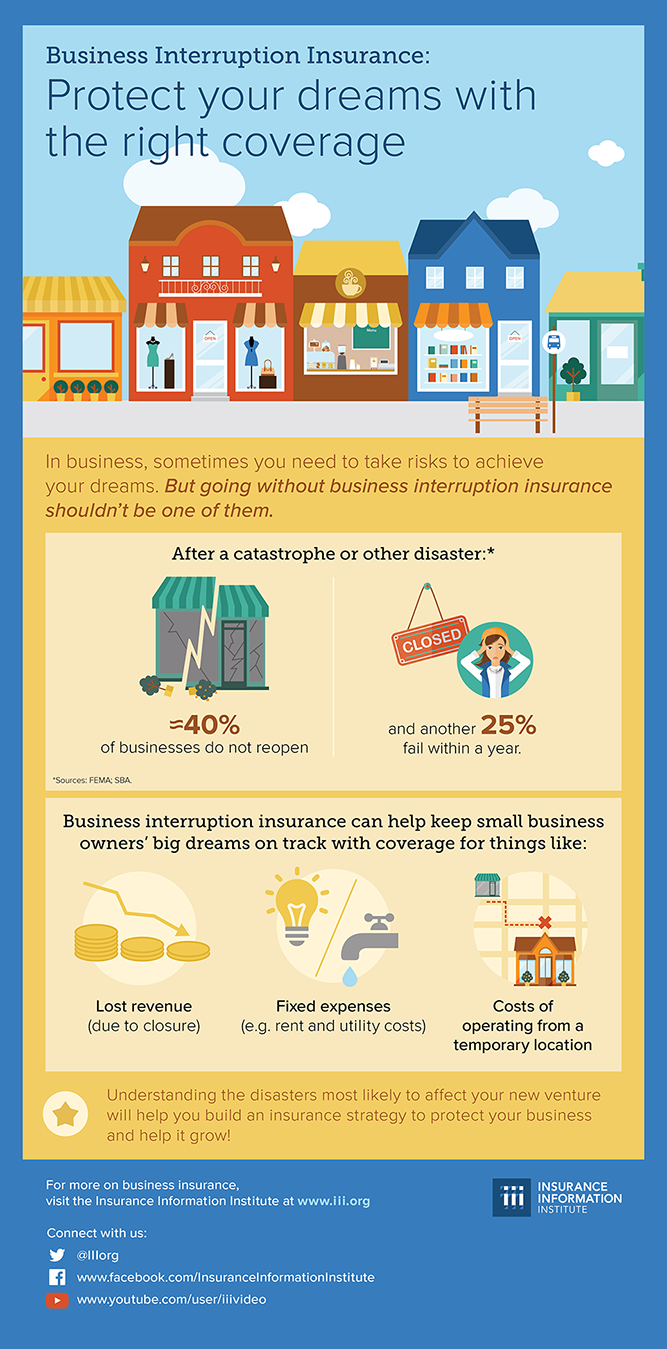

Business Interruption Insurance

Sometimes your daily business operations can be interrupted. You may experience a disaster, such as a flood or a hurricane. You may experience a cyber hack that includes ransomware.

Any number of issues can occur that could stop the daily operations of your business. Until you’re back up and running, you will need an insurance policy that can help you continue to have working capital and not lose money as a result. Business liability insurance is that coverage.

Malpractice Insurance

If you are a service industry such as a doctor or lawyer, you need a particular type of liability coverage called malpractice insurance. This insurance covers your business should you or an employee cause your client irreparable harm because of negligence.

Not all businesses have malpractice insurance. However, those that must carry it must do so by law. This law means even if you have a BOP, you would need this in addition as this protection is not already inside a BOP.

Should You Buy a BOP or Small Business Insurance a la Carte Style?

The answer to this question is it depends.

If your small business is just getting started and you need the basics to make sure you are covered by law, then a BOP will often be sufficient. However, as your business grows, you will likely need more insurance protection than a BOP policy can offer. The good news is you can have a BOP and still purchase other insurance policies.

While a BOP may have certain minimums and maximums based on the carrier and state, it will still cover a small business owners for general liability and property insurance throughout the life of the policy.

As you begin to hire employees and expand your services, you can add additional coverages as needed. The most important rule to a BOP is that once you go beyond a small business, it may be beneficial to purchase insurance coverages a la carte style.

To learn more about small business insurance coverage, contact the experts at Orchid Insurance at 772-257-7977. Our licensed professionals will be happy to answer any questions you have.